Arre yaar, it's March 2026 already? Your Form 16 will land in your inbox any day now, and that sinking feeling is starting — "How much tax will I lose this year?" Every salaried professional in India knows this March panic. The good news? You've still got time to save serious money before March 31.

I'm talking lakhs for some of you. But only if you make smart moves today, not tomorrow. This isn't some theoretical lecture—this is your step-by-step survival guide written for regular salaried folks like software engineers, bank employees, teachers, government workers, and middle managers earning ₹6 lakh to ₹25 lakh annually. No complex jargon, no confusing CA speak, just plain talk with real numbers.

Over the next few minutes, I'll show you exactly which tax regime saves you more under the new FY 2025-26 rules, what you can STILL invest in right now, common traps that cost people thousands, and a 7-day action plan to beat the deadline. Let's dive in.

Key Takeaways

- Act Fast: March 31st is the absolute deadline for FY 2025-26 tax savings. No exceptions.

- New Regime Dominates: For most salaried individuals (especially those earning ₹6L-₹25L CTC), the New Tax Regime is now significantly more beneficial due to lower slab rates and a ₹12.75 Lakh tax-free limit (with standard deduction).

- Calculate Both: Always run the numbers for both Old vs. New regime based on your specific deductions to pick the winner. Don't guess.

- ELSS for 80C: If the Old Regime works for you, ELSS Mutual Funds are the fastest, most profitable, and most convenient way to maximize your ₹1.5 Lakh 80C deduction online before the deadline.

- Corporate NPS is Key: Actively explore and leverage your employer's NPS contribution (up to 14% of basic salary) as it's tax-free in both regimes and adds a substantial tax benefit.

- Avoid Panic Buying: Invest wisely; don't make last-minute poor financial decisions like high-cost ULIPs or long-term endowment plans solely for tax saving.

Table of Contents

- First Things First: What Are These Two Regimes?

- The Tax Slabs — Your Money Blueprint

- 8 Real-Life Scenarios: Who Wins and By How Much?

- Your Last-Minute 80C Arsenal (Invest TODAY!)

- Beyond 80C: Section 80D and NPS

- 10 Deadly Tax-Saving Mistakes (And How to Avoid Them)

- Your 7-Day Emergency Action Plan

- Frequently Asked Questions

First Things First: What Are These Two Regimes?

Think of it like choosing between two different restaurants.

The Old Regime is like your favorite traditional dhaba. The menu prices (tax rates) are higher, but you get massive discounts if you order the full thali with all the add-ons (deductions like 80C, 80D, HRA, home loan). However, you need to show receipts and proofs to the manager to claim every single discount.

The New Regime is like a modern, streamlined food court. The prices are lower across the board, but there are virtually no discounts. You get a flat standard deduction of ₹75,000 and your employer's NPS contribution, and that's it. Less paperwork, simpler math.

Since Budget 2023, the new regime is your default. But you can successfully switch to the old regime when filing your ITR by July 2026. Smart taxpayers run both calculations and simply pick the winner.

The Tax Slabs — Your Money Blueprint for FY 2025-26

If you want to save money, you need to know the rules of the game. Here are the exact, updated rates for salaried individuals under 60 years for the current financial year:

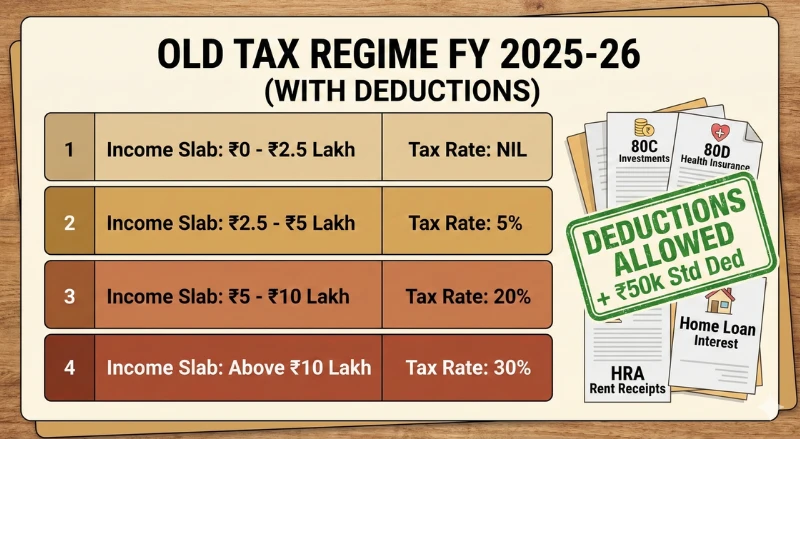

OLD TAX REGIME (The Deduction Heavyweight)

| Income Slab | Tax Rate |

|---|---|

| Up to ₹2.5 Lakh | Nil |

| ₹2.5 Lakh to ₹5 Lakh | 5% |

| ₹5 Lakh to ₹10 Lakh | 20% |

| Above ₹10 Lakh | 30% |

Plus: ₹50,000 standard deduction + every 80C/80D/HRA deduction you can legally claim.

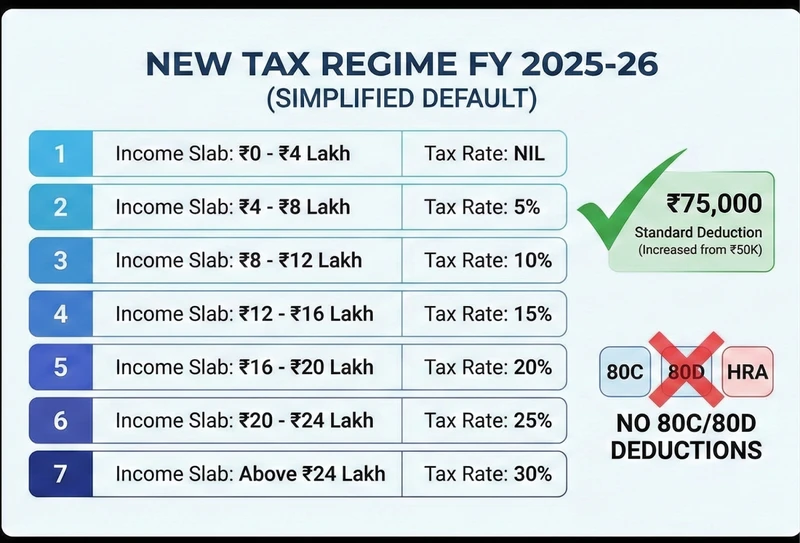

NEW TAX REGIME (The 2025-26 Simplified Slabs)

| Income Slab | Tax Rate |

|---|---|

| Up to ₹3 Lakh | Nil |

| ₹3 Lakh to ₹6 Lakh | 5% |

| ₹6 Lakh to ₹9 Lakh | 10% |

| ₹9 Lakh to ₹12 Lakh | 15% |

| ₹12 Lakh to ₹15 Lakh | 20% |

| Above ₹15 Lakh | 30% |

Plus: ₹75,000 standard deduction + employer's NPS contribution.

🔥 The 2026 Game-Changer (Section 87A): Under the New Regime, if your total taxable income is up to ₹12 Lakh, you get a full tax rebate. With the ₹75,000 standard deduction, this means a salary of ₹12.75 Lakh is 100% TAX-FREE without showing a single investment proof!

8 Real-Life Scenarios: Who Wins and By How Much?

Don't trust theory. As a financial professional, I see the actual numbers. Let's look at real salaried employees:

Scenario 1: The Fresher (₹8 Lakh CTC)

Ankit, 24, IT Support (Lives with parents, no rent)

- Old Regime: ₹7.5L taxable (after 50k std ded). Tax = ₹62,500.

- New Regime: ₹7.25L taxable. Falls under the ₹12L limit. Tax = ₹0.

Winner: New Regime (Saves ₹62,500)

Scenario 2: Mid-Level with Rent (₹12 Lakh CTC)

Neha, 29, Marketing Executive (Pays ₹18K rent in Lucknow)

- Old Regime: HRA ₹1.8L + 80C ₹1.5L + Std Ded ₹50K = ₹3.8L off. Taxable: ₹8.2L. Tax = ₹76,500.

- New Regime: Only ₹75K std ded. Taxable: ₹11.25L. Falls under the ₹12L limit! Tax = ₹0.

Winner: New Regime (Saves ₹76,500)

Scenario 3: The Heavy Investor (₹16 Lakh CTC)

Vikram, 32, Project Manager

- Old Regime: Max 80C ₹1.5L + 80D ₹25K + HRA ₹2L + NPS ₹50K + Std Ded ₹50K = ₹4.75L off. Taxable: ₹11.25L. Tax = ₹1,50,000.

- New Regime: Taxable ₹15.25L. Tax = ₹1,08,750.

Winner: New Regime (Saves ₹41,250)

Scenario 4: The Homeowner (₹22 Lakh CTC)

Pooja, 36, Bank PO (Has a large home loan)

- Old Regime: Home loan principal ₹1.5L + interest ₹2L + 80D ₹50K + HRA/LTA ₹1.5L + Std Ded ₹50K = ₹6L off. Taxable: ₹16L. Tax = ₹2,92,500.

- New Regime: Taxable ₹21.25L. Tax = ₹2,31,250.

Winner: New Regime (Saves ₹61,250)

💡 The 2026 Golden Rule: The New Regime is now incredibly powerful. Unless your total deductions (HRA, Home Loan Interest, 80C, 80D, NPS) are crossing ₹4.25 Lakh to ₹5 Lakh, the New Regime will almost always put more money in your bank account.

Your Last-Minute 80C Arsenal (Invest TODAY!)

If you run the math and find the Old Regime works better for you, you need to maximize your Section 80C Limit (₹1.5 Lakh) immediately. FY26 ends on March 31st. Here is what works best:

-

ELSS Mutual Funds — The Last-Minute Champion

Why it's the best: It has a 3-year lock-in (the shortest of all tax savers) and historical returns of 12-18%.

How to execute: Contact us for immediate ELSS portfolio allocation. As a registered distributor, we ensure your investment is processed today so you get the PDF proof for your HR department immediately.

The Wealth Factor: ₹1.5L invested today at 15% becomes roughly ₹6 Lakh in 10 years. An FD will barely cross ₹3 Lakh.

-

Public Provident Fund (PPF)

Safe, government-backed, with guaranteed 7.1% returns. You can add to your existing account via your bank's net banking portal (max ₹1.5L/year). Remember, it has a 15-year lock-in, so this is strictly for long-term debt allocation.

-

5-Year Tax-Saving Fixed Deposits

Every major bank offers these. Current rates hover around 7-7.5%. They are incredibly safe but will barely beat inflation after taxes. Good for conservative investors who need a quick fix before March 31.

-

Sukanya Samriddhi Yojana

If you have a girl child under 10 years old, this is a brilliant debt instrument offering 8.2% returns.

Beyond 80C: Section 80D and NPS

Health Insurance (Section 80D - ₹75K Deduction)

One hospital bill can wipe out three years of your meticulously planned tax savings. Securing health insurance is non-negotiable.

- Self + Family (under 60): ₹25,000 deduction.

- Parents (under 60): Additional ₹25,000.

- Parents (60+): Additional ₹50,000.

Action: Contact us today to get the best family floater policy with a strong cashless network in Lucknow. We provide instant policy issuance for your tax proofs.

NPS — The Hidden Gem (Works in BOTH Regimes!)

- Tier 1 NPS (Your Contribution): Under the old regime, you get ₹1.5L (80C) + an exclusive ₹50K extra under 80CCD(1B) = ₹2L total.

- Tier 1 NPS (Employer's Contribution): This is the ultimate hack. Up to 14% of your basic salary contributed by your employer is tax-free in BOTH regimes!

Action: Ask your HR about corporate NPS. For your personal ₹50,000 extra deduction, message us to open your NPS account within 24 hours.

HRA Exemption: The Rent Payer's Secret Weapon

If you live in a Tier-2 city like Lucknow, calculating HRA requires attention to detail. The exemption is the least of these three:

- Actual HRA received from your employer.

- Rent paid minus 10% of your basic salary.

- 40% of your basic salary (It's 50% only for Metro cities like Delhi/Mumbai).

What you need by March 20: A valid rent agreement and 12 months of rent receipts. If rent exceeds ₹1 Lakh annually, you must provide your landlord's PAN card to your employer.

10 Deadly Tax-Saving Mistakes (And How to Avoid Them)

- "New regime means zero tax always." Wrong. It means zero tax only if your income is up to ₹12.75 Lakh. Beyond that, standard slab rates apply.

- Ignoring your employer's NPS. You are leaving up to ₹1 Lakh+ of free, tax-free money on the table annually.

- Investing in PPF blindly. The maximum limit is ₹1.5L per person. Check your existing balance before dumping more money in March.

- Missing the HR deadline. Employers usually cut off proof submission around mid-March. If you miss it, they will deduct TDS, and you'll have to wait until you file your ITR to claim a refund.

- Buying insurance from pushy agents. You often end up paying 2x the premium compared to buying a direct, online term or health plan.

- Using ULIPs as your primary 80C. They often yield 5-6% returns due to high mortality and administration charges, compared to an ELSS fund's 12-15%.

- Thinking "High CTC = High Tax." It is your take-home and taxable income that matters. Structure your salary smartly.

- Forgetting children’s tuition fees. The tuition fee component of your child's school fees is 100% eligible under Section 80C.

- Not using employer medical reimbursements. Always submit those pharmacy bills if your company provides an allowance.

- Panic buying on March 30th. This leads to locking your money in terrible 20-year endowment policies just to save a few thousand rupees today.

Your 7-Day Emergency Action Plan

- 1Day 1 (Today): Download your latest salary slips. Use an online income tax calculator. Run the Old vs. New regime math using the FY 25-26 slabs above.

- 2Day 2: Email HR: "What is the status of my corporate NPS contribution? Can we opt-in?"

- 3Day 3: Calculate your 80C shortfall. Contact us to make a lump sum ELSS investment online to bridge the gap.

- 4Day 4: Renew your health insurance and scan your rent receipts/landlord PAN.

- 5Day 5: Download your Home Loan interest certificate (Form 16A) from your bank's net banking portal.

- 6Day 6: Submit ALL proofs in a single, organized PDF to your employer/HR portal.

- 7Day 7: Double-check your March payslip to ensure the TDS deduction has dropped. Relax until ITR season!

Final Words — Your 3-Point Mantra

- Calculate BOTH regimes using actual math. Don't guess. The new 2026 rules have flipped the script, making the New Regime vastly superior for 80% of salaried professionals.

- Use ELSS today if you need 80C. It is the quickest, most profitable way to hit your ₹1.5 Lakh limit online.

- Talk to HR about Corporate NPS. That 14% basic salary exemption is sitting there waiting to be claimed.

You now have everything you need to save ₹25,000 to ₹1.5 Lakh before March 31. But reading this article won't save you a single rupee—implementation will. Get in touch with us today to finalize your tax-saving investments.

Disclaimer: This guide is for educational and informational purposes only and does not constitute personalized financial or tax advice. Please consult a qualified Chartered Accountant (CA) before filing your returns.

Frequently Asked Questions

Can I invest in 80C after March 31 for this year's taxes?

No. The financial year permanently closes on March 31. Investments made on April 1, 2026, will count toward the next financial year (FY 2026-27).

Is the New Regime better for job switchers?

Yes! It offers a clean slate with no hassle of transferring rent receipts, investment proofs, or previous employer TDS certificates to your new HR department, simplifying the process significantly.

What about Capital Gains tax?

Capital gains (like selling stocks or property) follow the same rules regardless of which regime you choose. Remember, Long-Term Capital Gains (LTCG) on equities up to ₹1.25 Lakh per year remain tax-exempt.

My wife is a homemaker. Can we split the tax burden?

You cannot legally split your salary income. However, you can invest money in her name (e.g., PPF or mutual funds) to build wealth. Do note that any income generated from money you gifted her will be clubbed with your income for tax purposes.

What happens if I miss the HR deadline for submitting proofs?

If you miss your employer's deadline for proof submission (typically mid-March), your employer will deduct TDS based on the assumption that you haven't made any tax-saving investments. You will still be able to claim all eligible deductions and exemptions when you file your Income Tax Return (ITR) by July 2026, but you'll have to wait for the refund.

Written By

Amit Kumar Dwivedi

AMFI Registered Mutual Fund Distributor (ARN-139499). Helping families in Lucknow build wealth through SIPs, Health Insurance, NPS, and smart planning.