Bhai, appraisal letter aaya? Congratulations! That 10-12% salary hike feels amazing, right? But here's the real boss move: don't let it all vanish into lifestyle inflation. Park that extra cash into a Step-Up SIP and watch your wealth double (or even triple) over the next 10-12 years.

If you're a salaried professional in Lucknow—an IT guy in Gomti Nagar, a Bank PO in Hazratganj, or a teacher in Aliganj—this guide is your exact financial blueprint. No complicated jargon, just simple steps, real numbers, the latest 2026 mutual fund data, and Lucknow-specific wealth tips.

By the end of FY 2026-27, you'll be laughing at your old savings account balance. Let's turn that hike into a ₹1 Crore corpus.

Key Takeaways

- Step-Up SIP is the Ultimate Wealth Hack: Automatically increasing your SIP by your appraisal percentage (e.g., 10%) annually lets you double your final corpus without extra effort.

- Beat Lifestyle Creep: Invest your hike before you spend it. This prevents weekend outings from eating into your long-term retirement dreams.

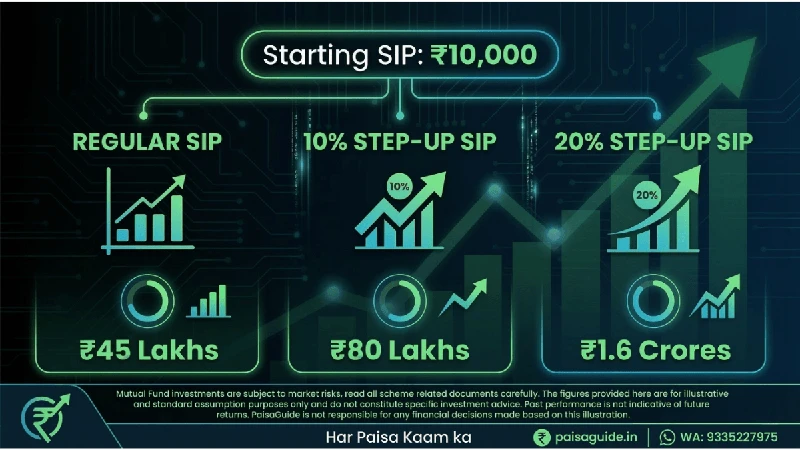

- The Power of 2026 Math: A ₹10k monthly SIP at 12% returns for 12 years yields ₹45L. The same SIP with a 10% annual Step-Up yields a massive ₹1.2 Crore!

- Automate for Consistency: Use an auto-mandate so you don't have to remember to increase your contribution manually every year. Set it and forget it.

Table of Contents

- What the Heck is a Step-Up SIP?

- Why Step-Up SIP is Perfect for Lucknow’s Salaried Folks

- The Math: Regular SIP vs. Step-Up SIP Calculator

- Top Mutual Funds for Step-Up SIP in 2026

- How to Set Up a Step-Up SIP in 5 Minutes

- Lucknow-Specific Tips to Maximize Your Hike

- 5 Common Mistakes Beginners Make (Avoid These!)

- Your 7-Day Action Plan Post-Appraisal

- The Bottom Line

- Frequently Asked Questions

What the Heck is a Step-Up SIP? (The 5-Min Explanation)

Regular SIP: You invest a fixed ₹10,000 every single month. It's safe, but it ignores the fact that your salary is growing every year.

Step-Up SIP: You start with the same ₹10,000, but you set an instruction to auto-increase it by 10% every year (or whatever percentage your appraisal was). Year 2: ₹11,000. Year 3: ₹12,100, and so on.

Why is this a genius move for appraisals? Your salary is likely jumping 9-12% in 2026 (the IT/BFSI average). By simply matching your SIP increase to your salary hike, you effortlessly double your wealth compared to a regular SIP, without feeling the pinch in your daily expenses.

The Quick Math

- Start: ₹10k/month (your current SIP)

- Appraisal: 10% hike → Step-up your SIP by 10% annually.

- After 12 years @ 12% returns:

- Regular SIP: ₹14.4L invested → ₹45L corpus

- Step-Up SIP: ₹25L invested → ₹1.2 Cr corpus!

Why Step-Up SIP is Perfect for Lucknow’s Salaried Folks

The Lucknow Reality Check:

- IT Sector (Gomti Nagar): Average salary hike in 2026 is 10-12% (AI/ML roles are seeing 15%+).

- BFSI (Hazratganj): Banking professionals are seeing steady 8-10% hikes.

The Problems a Step-Up SIP Solves:

- Lifestyle Creep: That extra ₹10k in your salary vanishes quickly on weekend outings in Biryani Nagar or expensive cafes.

- Zero Willpower Needed: We all forget to manually increase our investments. An auto-step-up mandate does the heavy lifting for you.

- Beating Inflation: With CPI inflation hovering around 6%, a 10% step-up ensures your investments are actually growing in real value.

- The Compounding Rocket: Pumping more money into the market during your early earning years leads to massive, exponential growth later.

Real Client Story: My client Ravi (working at an IT firm in Gomti Nagar) started a ₹15k SIP in 2023. After a 12% appraisal in 2026, he stepped it up by 10%. By 2035, his projected corpus is ₹2.1 Cr. If he had stuck to a regular SIP, he'd only be sitting on ₹85L.

The Math: Regular SIP vs. Step-Up SIP Calculator

Let's run YOUR numbers. We will assume a conservative 12% return (Even though the Nifty 5-year average is closer to 18%).

Case 1: The ₹10k Monthly SIP (Typical Lucknow Fresher Post-Appraisal)

Winner: Even a modest 10% step-up nearly doubles your final wealth!

(Pro Tip: Reach out to us at PaisaGuide.in, and we will run a custom Step-Up projection based on your exact age, risk profile, and current portfolio! Or use our tool below.)

Step-Up Calculator →Case 2: The ₹20k SIP (Mid-Level Professional, ₹12L+ CTC)

- Regular SIP: ₹28.8L invested → ₹90L corpus

- Step-Up 10%: ₹51L invested → ₹1.6 Cr corpus

Bonus Wealth: You create an extra ₹70 Lakhs just by increasing your contribution alongside your salary!

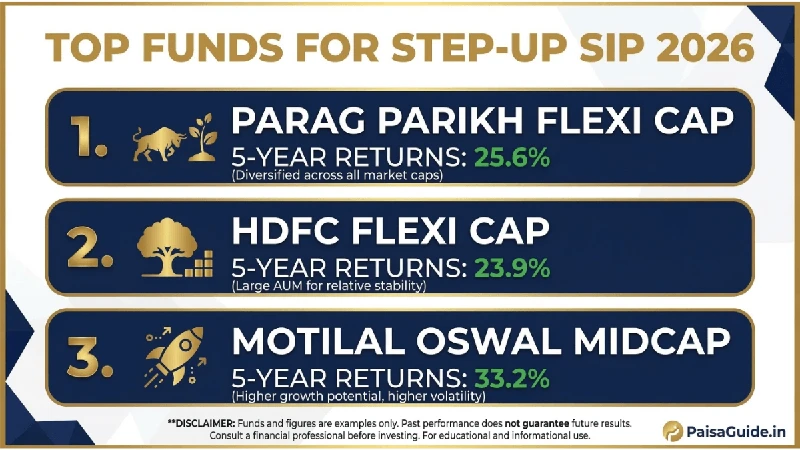

Top Mutual Funds for Step-Up SIP in 2026 (Latest Data)

For beginners, the golden rule is Flexi Cap + Large Cap. This gives you the best balance of stability (60% large-cap) and growth (40% mid/small-cap).

Important Note: A fund that worked great for your colleague might not be right for your specific goals. At PaisaGuide, we analyze your complete financial picture before recommending the exact fund mix for your Step-Up SIP.

How to Set Up a Step-Up SIP in 5 Minutes (The PaisaGuide Way)

Many investors try to do this themselves on direct apps, pick the wrong highly-volatile fund based on recent returns, and end up stopping their SIPs during market crashes. Here is how you do it the right way, with professional guidance:

- Contact Us: Drop a message to PaisaGuide.in.

- Portfolio Alignment: We review your risk appetite and select the perfect fund combination (e.g., Flexi + Large Cap).

- We Do the Heavy Lifting: We generate the secure Step-Up SIP link and send it directly to your phone/email.

- Set Your Limit: You choose the initial amount (e.g., ₹10k) and the annual step-up percentage (e.g., 10%).

- Approve the Mandate: You approve the bank mandate securely online. Done!

We monitor the portfolio year-round, ensuring your money is always working as hard as you do.

📈 New Financial Year Special Offer

Start or Step-Up your SIP with expert guidance. Get a free portfolio review today.

Get Your Free Portfolio Review →Lucknow-Specific Tips to Maximize Your Hike

- Gomti Nagar IT Pros (10-15% hikes): If your salary jumps from ₹10L to ₹11.5L, you have an extra ₹1.2L a year. Use that to step up your SIP by 12-15%. It will easily outpace the high PG and flat rents in the area.

- Hazratganj Bankers (8-10% hikes): Combine a Step-Up SIP with your corporate NPS. It’s a double whammy of tax-free growth and compounding wealth.

- Aliganj Teachers/Govt Staff (7-9% hikes): You have highly stable, predictable hikes. Let us pair a conservative 8% step-up in a Large Cap fund with your existing Post Office schemes.

5 Common Mistakes Beginners Make (Avoid These!)

- Mistake: Stepping up too aggressively (e.g., 25% a year). You won't be able to sustain it when expenses rise. Fix: Match your exact appraisal percentage.

- Mistake: Putting your entire Step-Up into Small Cap funds chasing last year's returns. Fix: Let a certified distributor structure a balanced 60% Flexi/Large Cap allocation.

- Mistake: Promising to "do it manually" every year instead of automating. Fix: Set an auto-mandate on day one.

- Mistake: Stopping the SIP during a market correction. Fix: With an advisor by your side, you stick to the plan and let Rupee Cost Averaging work its magic when the market is down.

- Mistake: Starting a Step-Up SIP without an emergency fund. Fix: Build 3-6 months of expenses in a liquid fund first.

Your 7-Day Action Plan Post-Appraisal

- Day 1: Calculate your exact monthly hike amount. Decide your Step-Up %.

- Day 2: Check your emergency fund (Aim for ₹3-6 Lakhs).

- Day 3: Contact PaisaGuide.in to review your current portfolio and select your core funds.

- Day 4: Approve the Step-Up SIP mandate link we send you.

- Day 5: Tell your family—financial transparency is a flex!

- Day 6: Track the first auto-debit to ensure it goes through.

- Day 7: Celebrate your smart choice with some controlled Biryani!

The Bottom Line: Turn That Hike Into a Crore Today

Your appraisal is not just extra weekend spending money—it is your ultimate wealth fuel. By simply stepping up your SIP by 10-15% right now, you are taking the absolute easiest path to doubling your wealth over the next decade.

Bro, don't let that hard-earned hike vanish into lifestyle inflation. Treat it like the wealth accelerator it is. Drop a WhatsApp message to us at 9335227975 today, and let PaisaGuide.in handle the entire Step-Up setup for you. Because as we always say: Har Paisa, Kaam Ka! The 2036 version of you is going to look at your portfolio and high-five you for making this choice today. Let’s get to work!

Ready to double your wealth in FY 2026-27?

Drop a message to us and let PaisaGuide handle the setup for you.

Frequently Asked Questions

What is the main difference between a Regular SIP and a Step-Up SIP?

A Regular SIP involves investing a fixed amount monthly. A Step-Up SIP automatically increases this contribution by a percentage (like 10%) every year, matching your annual appraisal hike to boost compounding significantly.

How often should I step up my SIP and by what percentage?

You should aim to step up your SIP annually after receiving your appraisal. The percentage increase should ideally match your salary hike percentage (e.g., if you get a 10% hike, step up your SIP by 10% to beat lifestyle inflation).

Can I increase my SIP amount manually in an existing fund?

Yes, you can increase it manually, but automating it via a 'Step-Up' mandate is better. It removes manual effort and ensures you invest before you spend your salary hike.

Is Step-Up SIP better than starting a new SIP every year?

Yes, it is often more convenient as it keeps your portfolio clean with fewer folios while still giving you the benefit of increased compounding on your base investment.

What if I cannot sustain the Step-Up percentage next year?

Most platforms allow you to cap the step-up or pause it. The important thing is to continue the base SIP to maintain the benefit of long-term wealth creation.

Should I have an emergency fund before starting a Step-Up SIP?

Yes, absolutely. Building an emergency fund equivalent to 3-6 months of your essential expenses, stored in a liquid fund, is a crucial first step.

Written By

Amit Kumar Dwivedi

AMFI Registered Mutual Fund Distributor (ARN-139499). Helping families in Lucknow build wealth through SIPs, Health Insurance, NPS, and smart planning.